The “Invisible Hand” of Money Illusion

Part One

This post was rather long so I have divided into a three part series published sequentially.

Every individual... neither intends to promote the public interest, nor knows how much he is promoting it... he intends only his own security; and by directing that industry in such a manner as its produce may be of the greatest value, he intends only his own gain, and he is in this, as in many other cases, led by an invisible hand to promote an end which was no part of his intention.

- Adam Smith, The Wealth Of Nations

By a continuing process of inflation, governments can confiscate, secretly and unobserved, an important part of the wealth of their citizens.”

- John Maynard Keynes - The Economic Consequences of the Peace

I. Introduction

The title of this monograph is a reference to Adam Smith’s famous observation of the “invisible hand” of capitalism whereby individuals pursuing their narrow self-interests through free market exchange can lead (mostly) to the greatest good for the broader economy and society as a whole. He called it “invisible” because the mere observation of individuals all acting to profit themselves obscures the symbiotic outcome of their efforts for the public interest. (I choose to inject the qualifier “mostly” because the “greatest good” does depend somewhat on the assumptions of perfect competition in markets.)

Smith’s Invisible Hand is the linchpin of his arguments in support of free markets. However, the assumptions of perfect competition—open access and transparency—are critical and one might argue that in the absence of these conditions, the outcome can be far from beneficial for all. This is the focus of this essay where I address the hidden manipulation of markets in money and credit to promote what has become a form of “money illusion,” where the value denoted by the price of a good or service is no longer what we expect it to be, i.e. at the point where price intersects value. This directly affects our financial behavior. We naturally assume price denotes value, but they can, and often do, diverge. If one is unsure of true value (which can vary widely from person to person), the market price can easily under or overstate it. What follows is a comprehensive but rudimentary explanation of the deceptive, invisible hand of money illusion. (If well-versed in finance, the reader can skip over the technical simplifications that follow; but this essay intends to make a policy argument that requires some rudimentary technical analysis.)

In non-technical terms, money illusion is a strategy deployed by financial and governing elites to exploit, wittingly or unwittingly, asymmetrical information and human behavioral weaknesses in order to manage economic relations and markets. As I will explain in greater detail, money illusion is enabled by fiat currencies that remove constraints on the supply and price of credit that governments can issue and spend. This allows the money supply to increase separate from the stock of wealth it is meant to measure. In other words, money becomes the illusion. This need not be as nefarious as it sounds as many of these elites believe they are doing what is necessary to stabilize society in order for it to prosper over the long-term. It just so happens that the benefits accrue primarily to what elites see as their own productive efforts, which benefits those in power.

Despite the best intentions, we see the negative results all around us: policies that favor speculation and debt leverage to the detriment of producing, saving, and investing; a consumption-driven economy funded by cheap credit and excessive consumer debt rather than production and investment; the proliferation of imprudent “keeping up with the Joneses” behavior like YOLO (You Only Live Once) and FOMO (Fear of Missing Out).

Under the spell of money illusion, we have witnessed a bifurcation of society into the haves and have-nots – a divide between those who own and control financial and real assets versus those who depend upon wage incomes. Most seriously, we are experiencing the breakdown of the social contract and trust in democratic institutions and a lack of faith in market capitalism across the globe. What it adds up to is a form of financial “nihilism” that stems from the manipulation of money and distortion of economic value and moral values.

There are numerous dimensions to this analysis of money illusion, including price inflation, currency depreciation and devaluation[1], financialization, debt leveraging, tax policies, the domestic and international monetary regime, stock and bond markets, sovereign debt, fiscal spending, housing markets, statistical measures, political messaging, and political conflict. Let’s first start with what money is and what value is, versus how it is often perceived.

II. Money and Prices

We should start by defining money, which I have done at length in a previous essay “What is Money?” The short answer is that money is a unit of account—like a ruler—that is intended to measure relative values among goods, services, and assets. You see your house, your car or your salary representing value relative to other goods and services. What, then, is value? Value is a subjective measure that varies from person to person: I place a high value on classic (not classical) guitars and time to play them, but others might place greater value on a house or a particular automobile, or a luxury vacation. I would argue that true value, regardless of relative wants, is the freedom to spend your time and energy on whatever it is that gives your life meaning.[1]

But in order to trade value—say, trade one of my guitars for a vacation in Tahiti—we need some consistent comparative measure that we can trust. That would be money, a proxy functioning as a unit of account, a medium of exchange, and a store of value. This is the economist’s functional definition of money as a currency. Since money is a reference point, this raises the next question: how do we ‘value’ money itself as an entity separate from its proxy role? This is determined theoretically by the ratio of money currency relative to the supply of all the goods and services it can be traded for.

To unpack this, we will have to consider that there are many different money currencies that vary across sovereign nation-states. For simplicity we will use the US dollar (US$) as our reference. Many people don’t realize that they can’t buy anything and everything in the world with a US$. One cannot buy French wine with US$s. Somewhere along the chain of transactions, someone had to exchange US$s for Euros in order to buy and consume that French Bordeaux.

The value of the US$ then is the sum of all the goods, services, and assets denominated in US$ divided by the total supply of US$ in circulation. (In practical terms there are many different definitions of the money supply, but for our purposes here it includes the supply of dollar bank reserves and deposits that includes all the credits extended by banks and non-bank entities because lending money expands the supply of credit and thus the effective money supply.)

It’s important to make a fine distinction between money and credit. Money, unlike credit, settles transactions—once you pay with money (currency or a real asset like gold coins), the transaction is complete. Credit, on the other hand incurs a debt liability that must be repaid in the future, usually with interest. Such credits can be created by mutual agreement of any willing parties. Credit produces new buying power borrowed from the future, without necessarily creating new wealth. It allows borrowers to spend or invest more than they earn, pushing up demand and prices. The debt obligation requires borrowers, who are now debtors, to spend less than they earn to pay back their debts. This reduces demand and prices in the future. Essentially the idea of credit and debt is to reallocate and shift savings, consumption, and investment over time with the intention of creating more new wealth than the debt incurs. Ideally.

We can see here that the supply of money can vary from the sum total of all the assets it is meant to represent. If we double the supply of money but the sum total of produced goods and services remains the same, then the real value that the dollar is supposed to represent is cut in half in US$ terms.

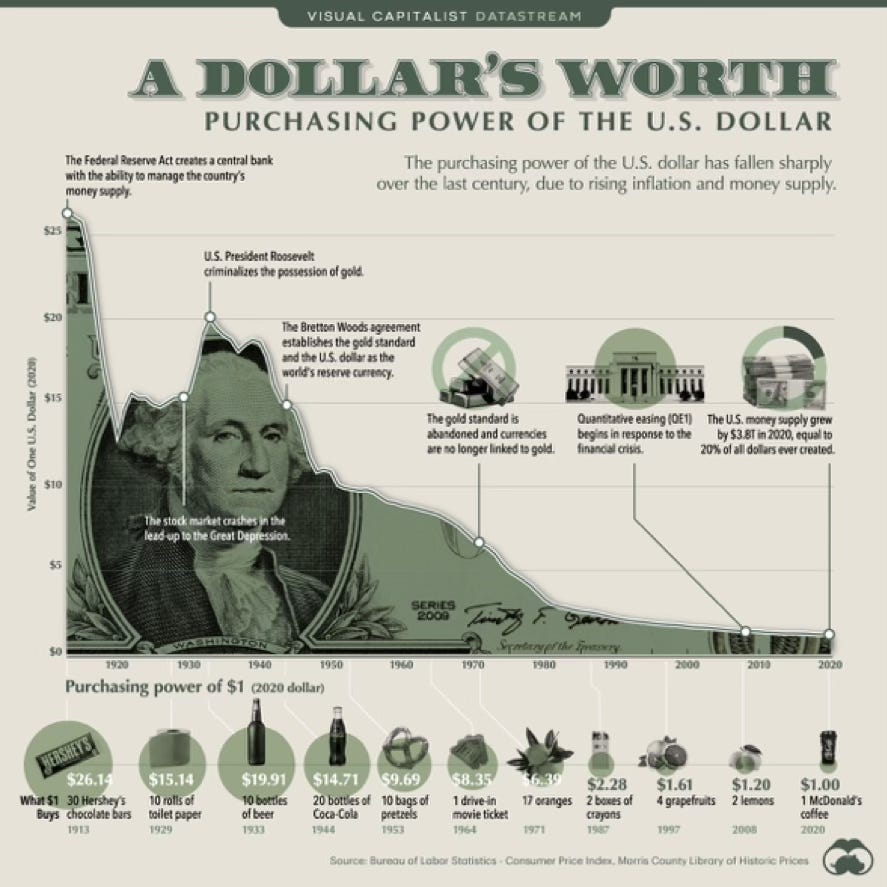

The accompanying graph illustrates this decline in the purchasing power of the US$ over the past century. Without trying to explain the ups and downs of the chart, suffice to say that in real terms $26 today will buy you what $1 would buy back in 1913—that $1 million mansion your robber baron great grandfather bought in 1913 would cost $26 million today. What we see here is a devaluation of the “price” of US$ in terms of what it can be exchanged for. This is an accurate description of price inflation and currency devaluation, which are flip sides of the same coin.

One might ask how can and does this happen? It can happen because money is not a “good” in itself, but just a measuring unit for the value of something else. If we decide that one foot is now 20 inches, our 6’ height as measured in inches goes from 72 in. to 120 in, but our true height hasn’t changed at all. If the supply of money is not held constant relative to the supply of goods and services, only the unit of measurement has changed. Now we’re getting to see how money illusion can create a misreading of true value. How this happens depends on who or what controls the money supply.

Money Supply

In the world today we have hierarchical, centralized control of the supply of different monies, or currencies. Most countries have an institutionalized central bank that somewhat controls the supply of money and credit denominated in the sovereign nation’s currency. In the US, this is the Federal Reserve Bank. In the UK it is the Bank of England, in Europe the European Central Bank (ECB) and so forth. We do not have a free, competitive market in money and credit and this is where we depart from Adam Smith’s benevolent Invisible Hand of capitalist finance.

The central banks do not have total control of the money supply because of non-bank financial intermediaries that extend credit, such as mortgage, insurance, and consumer credit companies, investment banks, money market funds, etc. This is referred to as the shadow banking system[1] that is not subject to the rules and regulations under any state banking system (the Federal Reserve system in the case of the US). This means that the Fed can leverage the US money supply and available credit through the fractional reserve US banking system, but cannot control the supply of US$ credit available through the global shadow banking system. This weakening control is true of all the central banks and has led to efforts to coordinate monetary policy in concert, led by the US Fed.

However, using its direct control over Federal Reserve system banks, the Fed exerts considerable power over the conduct of monetary policy in the US and across the world due to the US dollar’s role as the global reserve currency. Since 1970, Fed has increased the US$ M1[2] supply of currency and bank deposits from roughly $200 billion to more than $20 trillion during the pandemic—an increase of 100 times—while US GDP increased only 20 times, from roughly $1 trillion to $20 trillion. This means the supply of money exceeded the supply of things one can buy with that money by at least a factor of 5. Theoretically then, we can expect the purchasing power of those US$s to have fallen by a factor of 5 over the past 50 years. In a nutshell, this is why the nominal prices of real assets, such as houses, land, gold, energy, etc. have exploded, while median wages and incomes struggle to keep pace. If we adjust these prices for inflation we find that nominal prices have merely kept up with inflation to preserve the real value of the assets, so those nominal prices do not necessarily represent real increases in wealth.

Simply viewed, we see that borrowing of new credit to be invested over time in the economy is not providing a profitable return sufficient to pay back the debt with interest. It’s like you borrowed $400,000 for college, but now can’t find a job. We’re starting to get the picture here, but we still have a long way to go.

III. Inflation and Debt

As explained above, price inflation is really a measure of the devaluation of the currency in which price is quoted. Inflation is not a modern phenomenon as currencies have been devalued and debased for as long as they have existed. In the days of metal coinage, sovereigns used to shave or reduce the quantity of metal used in the coinage—a tactic known as seignorage. In the paper currency age this is accomplished by just printing more paper currency. In our digital age, the central banks just credit the reserves of member banks, essentially just changing a number on their balance sheets.

Now, why would they do that, knowing the result is to debase the currency? It’s easy to discern the motives for doing so. Money is created through credit creation, which when borrowed creates debts that must be paid back in the future. As we have seen a massive increase in the supply of credits through the Federal Reserve banking system, we have seen the explosion of new debt as these subsidized credits were borrowed in the private and public sectors of the economy. The US Treasury issues public debt to feed its deficit spending commitments as directed by the Congress’s power to tax and spend. In other words, politicians overpromise and governments overspend because they have no hard budget constraints like you and I have, but they do need to create more money credits to service the debt outstanding. The Federal Reserve either obliges the need to create more credit or risks a crisis of defaults in the credit markets.

One can observe this growth of US debt in real time at the US Debt Clock, where we can see the nation’s growing liabilities with current spending and borrowing policies. US Treasury debt has exploded from $370 million in 1970 to $36 trillion today – that’s an increase of one hundred thousand times!

We may notice from this chart that the acceleration in debt began around 1970. This is not a coincidence. In 1971 President Nixon issued an executive order to stop convertibility of the US$ into gold at $35/oz. This essentially ended the Bretton Woods peg of the US$ to gold, thereby transforming the international monetary system into a market-based floating exchange rate system. As we shall see, this has had profound consequences for the global economy over the past half century.

The best way to measure and compare debt across time is as a share of GDP. This is like comparing your total debt liabilities as a percentage of your income, from which you must service the interest payments on the debt. What matters more than the absolute percentage level is the trend over time—is it increasing or decreasing? As a share of GDP, US federal debt has been increasing from 34% in 1980 to 123% today. This means the return to our national income from borrowing has been dropping steadily to where new government borrowing returns less than the money borrowed to achieve it. Giving the increasing servicing costs of the debt, to keep pace with payment commitments borrowing must increase at an ever-increasing rate. This is an exponential function that eventually goes to the moon, or crashes. These are merely two different paths to the same destination—both routes are politically unacceptable.

Our policy-making elites are well aware of this dilemma since they managed to engineer it with their economic and financial policies over the past half century. They have been able to spend profligately because a fiat currency is merely an obligation for future payment—a promise—as opposed to a real asset that retains its value. When currencies were backed by convertibility to gold, deficit spending would lead to a drain of gold reserves as people redeemed their excess dollars for gold bullion. International trade deficits and surpluses would lead to gold flows among central banks, causing corrections through currency exchange rates. No more.

In a fiat currency regime, fiscal spending is unconstrained by hard budgets. This has allowed our international governing elites to spend more while taxing less, creating massive public deficits. As Ray Dalio writes in his new book How Countries Go Broke, some people believe that there isn’t any limit to government debt and debt growth, especially if a country has a reserve currency like the US. That’s because they believe the central bank of a reserve currency country that has its money widely accepted around the world can always print more to service its debts (and export its inflationary pressures). But there are consequences to this profligacy as the debt obligations must be serviced as the interest on the debt grows. Excessive government debt service crowds out other spending priorities as well as private sector borrowing and investment. This decline in private sector investment depresses long-term economic growth, while excess credit creation through the repression of interest rates leads to inefficient resource allocation and greater hidden systemic risks.

What options do policy-making authorities have to manage excess debt? The only viable political option is to depreciate the debt through money illusion while hoping nobody notices. The Federal Reserve deploys money illusion by depressing interest rates and manipulating bank reserves through quantitative easing, which means the Fed buys up outstanding public and private credits by expanding its balance sheet, injecting new credits into the financial system. It’s essentially writing blank checks on the national income and asset balance sheet.

In recent years, these tactics have financed fiscal deficits authorized by Congress and lent by the US Treasury through the sale of Treasury bonds, notes, and bills. The major buyer of US Treasury debt has become the Federal Reserve, rather than private investors, domestic and foreign. What we observe here is a vicious cycle of increased spending leading to increased debt that requires more spending and more debt to service the increasing quantity of debt liabilities. If this sounds a bit like a Ponzi scheme, that’s because it is. And all Ponzi schemes end up with a complete implosion, but the process of getting to that point imposes a host of negative social and economic effects along the way.

[1] A point of reference here. Depreciation refers to the decline in value of one currency against another. So, the US$ can depreciate against the Euro or Swiss Franc while appreciating against other currencies. Devaluation refers to the revaluing of the currency in terms of what it can buy. If your dollar buys less and less—gold, for instance—then it is being devalued.

[2] We should make a distinction here between money and wealth. Money is the measuring stick but wealth is the store of value that money ideally (i.e., without illusions) measures. While value is subjective and particular, the common denominator is time and energy.

[3] S&P Global estimates that, at end-2022, shadow banking held about $63 trillion in financial assets in major jurisdictions around the world, representing 78% of global GDP. This compares to about $7 trillion of assets currently on the Federal Reserve’s balance sheet.

[4] The accepted definition of M1 is currency in circulation and demand deposits (bank checking accounts). M1 does not include savings deposits or money market funds. It is the money supply aggregate where the Fed has the most direct control.